14 Reasons To Love YNAB

Nov 21, 2023

In my research on You Need a Budget (YNAB), I found few bloggers and reviewers writing about it. I was a little surprised because I knew YNAB had a cult following. Reddit turned out to be the source that made me want to give it a trial run. If you are on the fence about trying YNAB yourself, I hope this blog post convinces you to do it. As a budget nerd and paying user, I’m eager to share all the reasons I love using it!

You are not the product. YNAB doesn’t bombard you with ads and the company doesn’t sell your information to third parties. I like my privacy and am happy to pay for a high quality product.

The software is designed to only work with the money you already have. Many budgeting apps start with your total monthly income and have you budget out that amount. This is what I call guessing, and no one likes to have less money to spend than they expected. YNAB makes it difficult to overspend and will show alerts if you have overspent in a category. The red color drives me crazy and I do my best to go in and fix the overspending so I don’t have to see it. You want to work with accurate amounts in your budget.

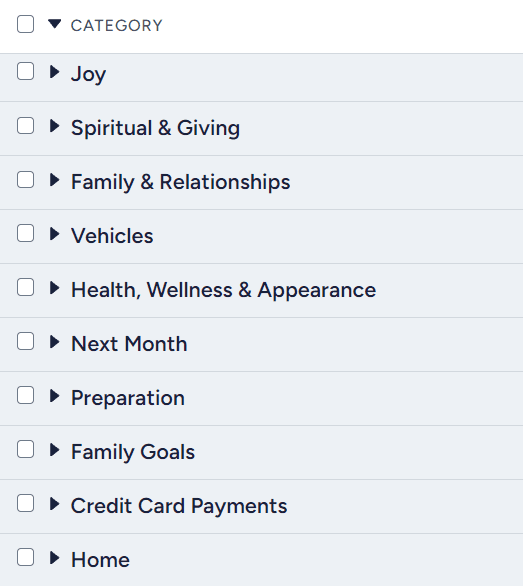

You can add and rearrange categories the way you want. Want to keep things super simple with 15 categories? Want 85 categories for your family of four? You aren’t limited to generic categories that don’t fit your lifestyle or priorities.

These are the category groups we currently use.

It incentivizes you to pay off and stay out of debt. For users paying their credit cards off every month, the app automatically assigns funds to pay the debt for you. And if you go over in credit spending, your available funds in the category and the banner at the top of your budget will turn red and prompt you to cover overspending.

The Age of Money feature can get you to save money. The whole idea is to increase the number of days between getting paid and spending money. I check my Age of Money every morning when I wake up. The higher the number ticks up, the more motivated I am not to spend unless it is a necessity. I’m way less likely to go hog wild on my credit card because that means the number will start dropping and it can take time to save up again. I no longer make impulse purchases thanks to this.

Up to 5 other family members can join and help you manage your budget using the YNAB Together feature. It helps keep everyone on the same page, and since it’s a web app changes happen in real time. You can also use YNAB on any device.

You can set up multiple budgets under the same subscription! I didn’t know about this feature until I was a few months into using the software. You could use it for a small business budget, your teenager’s budget, a “What if x happens?” simulator budget, etc.

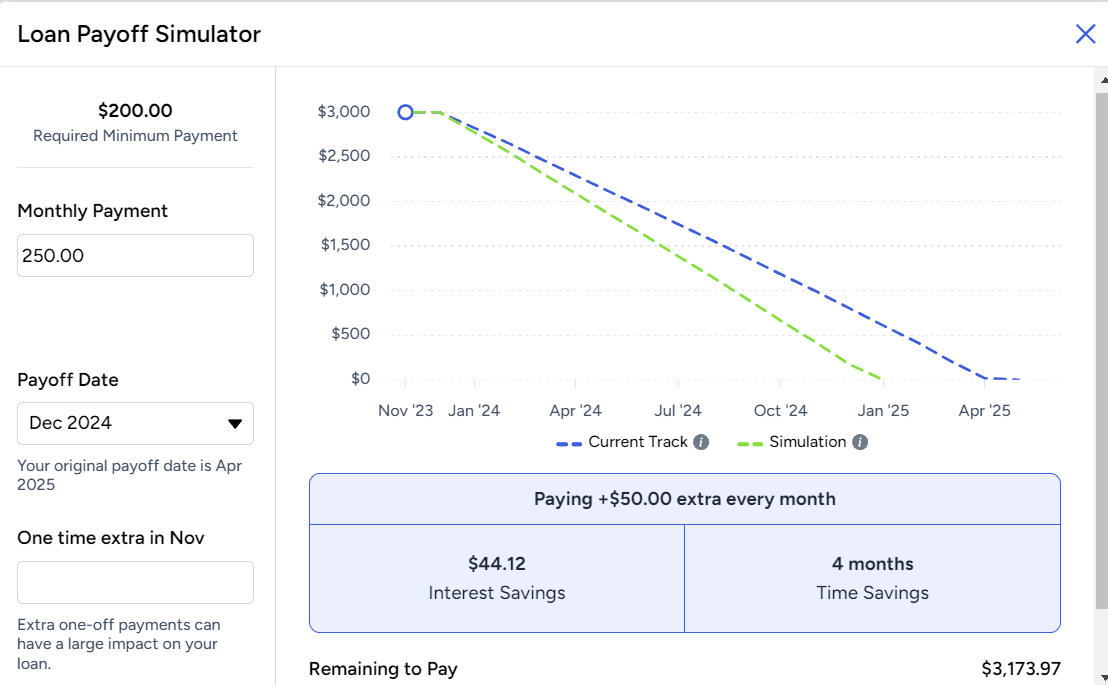

The app has a Loan Planner that is very fun to use. You can play around with increasing the amount you pay monthly and will see the new payoff date. You can even copy the new amount you want to pay monthly into your YNAB budget.

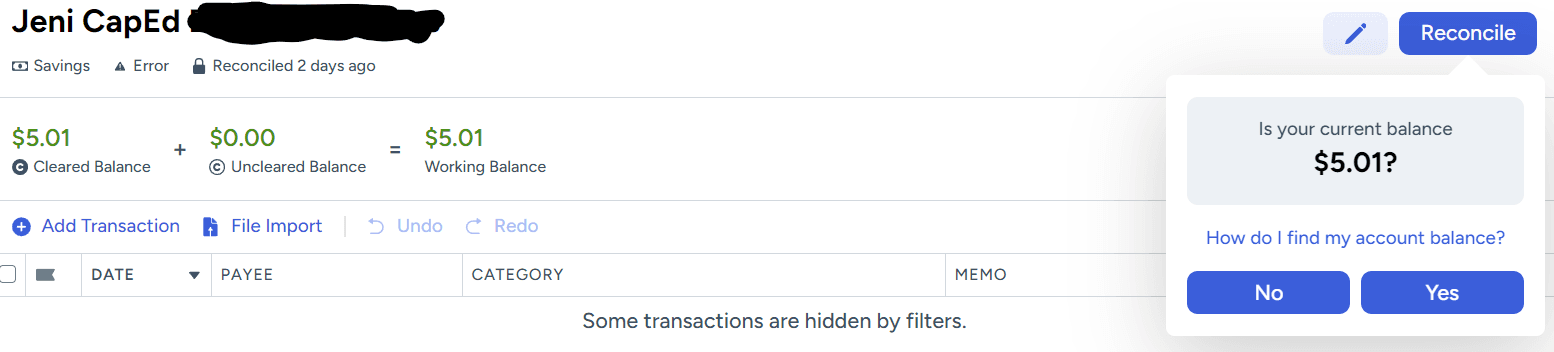

Reconciling accounts is a breeze. You can detect fraudulent or inaccurate transactions by using the reconciliation feature regularly. And if you make a mistake, you can undo an action! Remember balancing a checkbook? All the stress of getting it perfect is a thing of the past!

The UI/UX is great. Instead of using clunky bloatware, the interface is clean and attractive. And the product works as advertised. I wish more fintech apps were designed with the user in mind.

YNAB is easier to use than creating a spreadsheet budget. Trust me on this one! I have friends who do their own spreadsheets and I’ve tried (and failed) myself. I’m not an accountant and don’t really enjoy all the nuances of using spreadsheets. So YNAB does the heavy lifting, saving me a lot of time and headaches.

YNAB has extensive resources for people who want to learn. I find their YouTube channel, blog, podcasts and Reddit SO HELPFUL for YNAB newbies and nerds alike. There are also coaches you can meet with if you have questions about getting started or need support in the app.

It is proactive, not reactive. You decide what jobs you want your dollars to do upfront. Not say, “Oops, I spent $500 on Southwest tickets when my bills haven’t been paid yet. I probably shouldn’t have done that. Oh well, guess I’m terrible at budgeting!” after the fact. A zero-based budget makes it easy to see where your money goes each month. YNAB helped us realize we were on the credit card float and we could better fund our True Expenses.

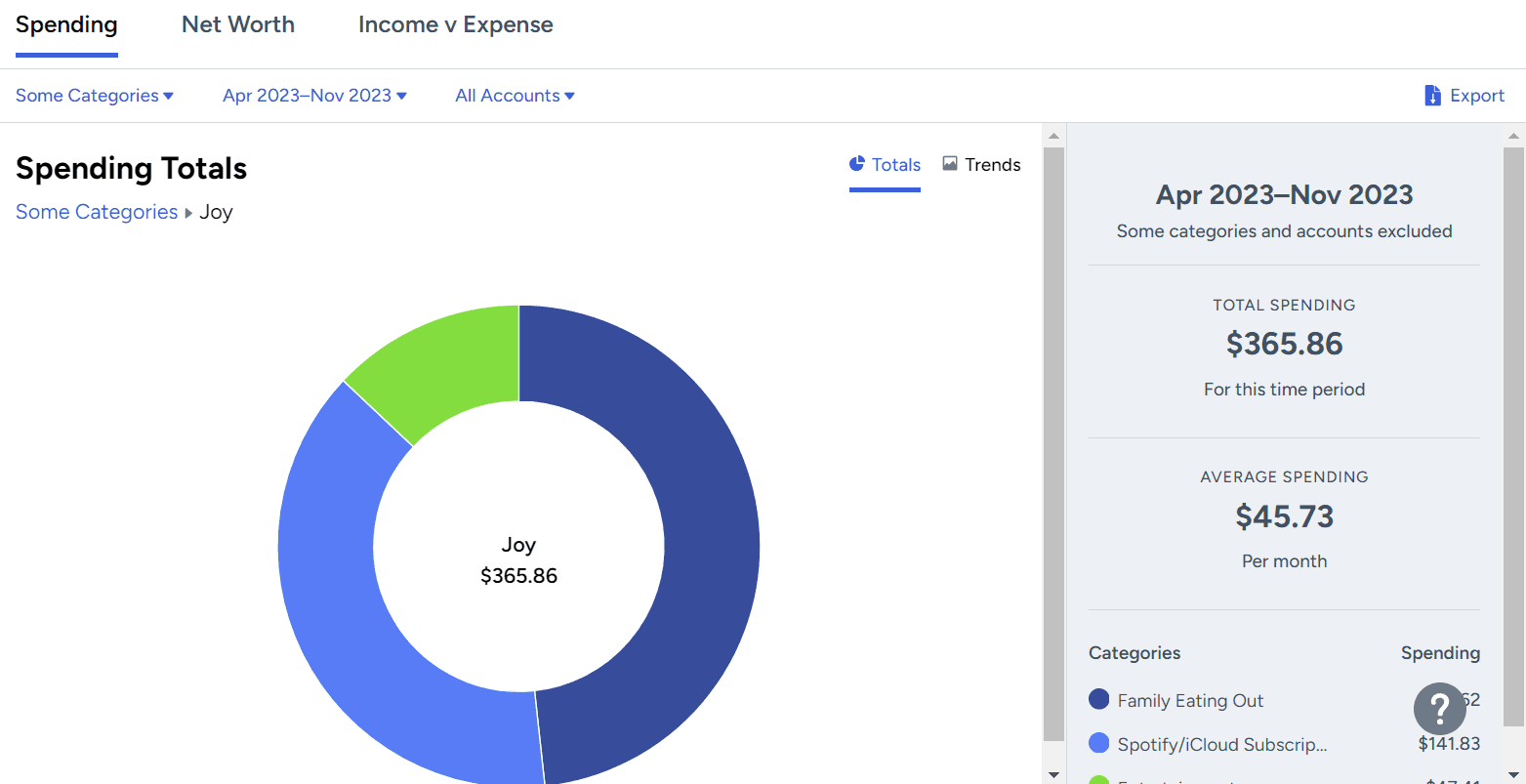

The Reports feature is informative and uncluttered. You can easily see how much you’ve spent in any category–the average you spend per month and what you spent in a specific period. I always thought we spent so much money on groceries until I checked Reports. Turns out we are better at meal planning and using up food in the fridge than I thought we were.

The Bottom Line

I encourage you to make the effort to trial YNAB as well and see your full financial picture in one place. While there is a learning curve (you will forget some things a week or even three months in), your efforts won’t be in vain. At the very least, you’ll know if you like getting into the nitty gritty of your finances or want to go a more relaxed route.

Helping clients regain control of their finances is my passion. If you want to learn basic or advanced budgeting, financial coaching might be a logical fit for you. Behavior change is a commitment and takes time, but don’t put off getting support if you need it. I’m happy to help!

Disclaimer: This is not a sponsored post. I am a paying user and not affiliated with YNAB in any way. As of this writing, YNAB offers a free trial for new users and the features mentioned in this blog post.